Compared to last year’s report, the story in 2026 is less about whether downtown activity will rebound through office recovery alone, and more about what the region’s “new normal” has become. Office leasing has fallen further, reaching the lowest level on record, and vacancy has continued to climb, reinforcing that hybrid work is not a temporary disruption but a lasting shift in demand.

Taken together, this year’s findings suggest that the path to recovery will depend less on restoring past commuting patterns and more on building a Central City that attracts a stronger mix of residents, visitors, and activity throughout the day and week.

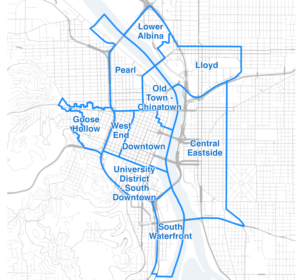

Report at a Glance

252,289

Quarterly average of leased square footage in 2025, lowest on record with exception to 2020.

86%

Total percent of foot traffic in Portland’s Central City compared to 2020 levels.

10.2 million

Quarterly average square feet of vacant office space in the Central City in 2025, highest level on record.

Economic Data

Portland’s quarterly office leasing fell from an averaged 400,000 square feet in 2024 to 250,000 square feet in 2025. This is the lowest level on record, below leasing activity during the 2020 pandemic, and far below the peak of 800,000 square feet per quarter averaged in 2014. See Figure 1.

Vacancy is moving in the opposite direction, with Portland’s Central City reporting the highest vacant office inventory on record. In 2025, vacancy averaged more than 10 million square feet and has increased steadily. It is projected to peak at the end of 2026 before gradually declining. See Figure 2.

Compared to its peer cities, Portland continues to see relatively strong residential foot traffic. This reflects, in part, the Central City’s larger geographic footprint, which creates greater opportunity for resident activity. It also reflects growth from a lower starting point: prior to the pandemic, Portland had the second lowest share of resident-generated foot traffic among its peers, leaving more room for residential presence to increase over time. That advantage may level off as housing construction slows. At the same time, Portland continues to trail its peers in both employee and visitor foot traffic. With office attendance largely stabilized and lease rates declining, meaningful gains in employee activity are unlikely. Visitor foot traffic therefore represents the greatest opportunity for growth and should remain a primary focus for downtown activation and amenities. See Figure 3.

Overall, Portland’s Central City foot traffic has recovered to about 86 percent of pre-pandemic levels, placing it near the middle of its peer group. Milwaukee is closest to a full recovery at roughly 92 percent, while Minneapolis continues to lag at about 83 percent of its pre-pandemic activity. See Figure 4.

Office attendance alone will not bring the Central City back to prior levels of activity. Even if workers returned to the office as often as they did before the pandemic, foot traffic would rise only modestly, with Downtown reaching about half of its former activity and South Waterfront coming closest to a full recovery. This reflects lasting changes in how people work and spend their time. Going forward, stronger visitor activity and a better mix of workers, residents, and visitors will matter more than a simple return to old commuting patterns. See Figure 5.

Conclusion

The data in this year’s report make clear that Portland’s Central City can no longer simply wait and hope for office demand to return. Record-low leasing, historically high vacancy, and stabilized work-from-home patterns point to a structural shift in how downtown space will be used going forward. At the same time, foot traffic has continued to recover, suggesting that downtown’s future will depend less on a full return to pre-pandemic commuting and more on creating a place that draws residents and visitors throughout the week.

Residential activity represents one of the clearest areas of opportunity for long-term growth, but that potential may be harder to realize as housing permitting and construction slow. The scale of vacant office space now represents one of the region’s defining challenges and opportunities. How Portland adapts this surplus, whether through reinvestment or reuse, will shape the vitality and economic role of Downtown and the Central City for years to come.

This report is presented to you by:

Value of Jobs Coalition Partners

Related Reports

June 2026

June 2026

The Economic Value of Recreation on the Willamette River, 2026

March 2026

March 2026

2026 State of Women in the Portland Metro Economy

February 2026

February 2026